May 2020

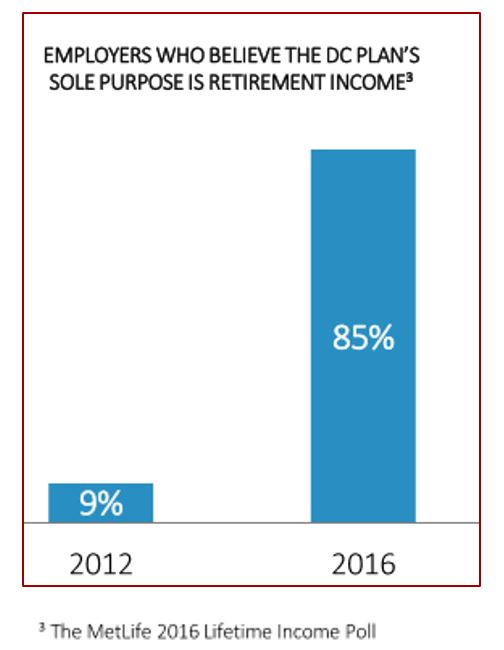

As the number of private pension plans continues to decline, companies are becoming more focused on employee financial wellness, including their ability to retire comfortably. This is critical as a 2018 Employee Benefit Research Institute (EBRI) Labor Force Participation Rate Brief identified that three out of four retirees plan to rely heavily on their assets accumulated in defined contribution plans during retirement1. Coincidentally, company attitudes seem to be shifting, illustrated by a recent Fidelity survey that identified 9 out of 10 plan sponsors feel responsible for supporting retiree spending needs2. Although seemingly altruistic, there are income statement related reasons for this orientation, as the same survey identified 90% of plan sponsors believe employees are often working beyond their anticipated retirement date in order to meet their financial needs during retirement. Generally speaking these long-tenured employees could be replaced by others just entering the labor market, with corresponding salary expectations and perhaps a more current skill set.

The burden to save for retirement is largely falling on a reluctant and ill-prepared plan participant base, who were previously able rely to on their employer-sponsored pension plan to provide substantial assistance for retirement income. In his book Nudge, Nobel Prize winning economist Richard Thaler compares this shift to someone who tries to cut their own hair—a mess5. While there have been volumes written about steps that can be undertaken (auto enrollment, re-enrollment, auto escalation, eliminating money market funds as default options), little new ground has been broken in these areas recently. Instead, the purpose of this paper is to point out a situation where best intentions could result in unintended consequences. Specifically, we’ll be reviewing plan architecture in terms of the number of options offered to plan participants.

"Can we ever have too much of a good thing?” wondered Miguel de Cervantes in Don Quixote. When it comes to retirement plan design the answer is an unequivocal yes. Let’s take a minute to revisit the Iyengar and Lepper “Jam Study” and discuss implications for retirement plans6. In 2000, the psychologists and study authors Sheena Iyengar and Mark Lepper conducted an experiment in consumer psychology at an upscale grocery store. The study is especially notable in terms of simplicity and equally insightful in its findings. For the uninformed, on one day the authors set up a display table featuring 24 varieties of gourmet jam. Those who sampled the jams received a coupon for $1 off any jam. Returning on another day, shoppers were exposed to a similar table. The only difference was that there were only six varieties of jam on display that day with a similar coupon offer. The authors found that the large display attracted significantly more visitors than the smaller one. However, when it came time to making a purchase decision, people who saw the large display were one-tenth as likely to buy as people who saw the small display. Customers of Costco now understand why they limit breadth while emphasizing depth. Interesting but irrelevant? Read on!

The phenomenon has been replicated in a variety of product categories, from chocolate to financial services to speed dating, and has come to be known as “The Paradox of Choice” or “Choice Overload.” The paradox exists because we naturally think more choices are better as more choices certainly satisfy more needs. However, an extensive number of choices can be demotivating, as more options require additional time and effort to make a choice, which not everyone is prepared to do. As Professor Iyengar noted, “the presence of choice might be appealing as a theory, but in reality people find more and more choice to actually be debilitating”. Applying the Choice Overload paradox to a 401(k) or 403(b) line-up, too many options may unintentionally place a psychological burden on plan participants because the opportunity to make a “wrong” choice is greater, which may ultimately result in choice deferral and subsequent (option) switching. We won’t even get into buyer’s remorse, regret and self-blaming!

The “Jam Study” has undergone a great deal of scrutiny over the years. A recent study “Choice Overload: A Conceptual Review and Meta-Analysis” by Kellogg researchers at Northwestern University has re-analyzed the data from 99 other Paradox of Choice studies and isolated when reducing choice is more likely to lead to optimal decision making7.

These include the following categories:

As the astute reader will note, the four qualifiers above can all be linked to retirement plan line-ups in various ways. Effort minimization may be a factor, as many plan participants might find themselves under time pressure (due to procrastination or other reasons) to enroll. For non-financial professionals, the complexity of the products themselves may make the task of making the decision challenging. An abundance of choices perceptibly leads to choice set complexity. Lastly, preference uncertainty is likely to be significant, especially for non-financial professionals.

Long time clients of DeMarche know we are generally proponents of streamlined investment menus. More specifically, we remind plan sponsors they are under no obligation to present plan participants with a myriad of options. In fact, doing so may invite potential litigation if any of these options are later deemed to be esoteric or in some way difficult for the average person to comprehend. The days of leaning on the prospectus language (many of which now exceed one hundred pages) as a defense are largely over. Instead of numerous and sometimes confusing options, we advocate the following:

For plans that seek exposure to high yield bonds and emerging market equities, identify broader strategies that include exposure to these markets tactically.

A well-conceived defined contribution plan can be one of the most compelling benefits for attracting and retaining valued staff—but only if your employees understand and take advantage of it. Removing complexity is an important step, as it lessens the likelihood of sub-optimal decisions and unintended consequences on the part of plan participants.