June 2020

“How long are we going to allow the underperformance of this manager to persist?” This has been a consistent investment committee conversation since, well, forever. The inherent costs of either making a decision to change or continuing on a potential path of underperformance can be difficult and divisive. The strong growth in equities since the Great Financial Crisis until mid-March 2020, along with the Black Swan that continues to lay eggs in 2020, has intensified the conversation regarding manager performance. In our practice we have found that investment committees spend an inordinate amount of time considering this question and many times find themselves “kicking it down the road,” hoping for improved performance or more decisive data that facilitates the choice to retain or terminate. In our February 2020 paper “Looking at Management Fees from a Different Perspective,” we made the following assertion related to investment manager/strategy selection and retention:

“We encourage emphasis on what we call the “leading indicators” of

future performance: stability of the manager’s firm, its ownership,

and leadership; stability of the investment management team; and

an appropriate growth/stability of the strategy’s assets under

management. Excess volatility in any of these fundamentals weakens

the odds of maintaining a winning strategy.”

- Tim Marchesi, CEO, CIO DeMarche

Since 1974, DeMarche clients have benefitted from forward looking research related to these “leading indicators.” The assertion is that disruption in one or more of these indicators can impact future performance and should be addressed as soon as observable. This paper will focus on validating that assertion. We will share primary research, specifically looking at the leading indicators of assets under management (AUM) volatility, philosophy/process changes, and manager turnover. We recognize that the leading indicators are inherently correlated and can be evidenced in concert as well as preceding or following one another.

A loss in assets under management (AUM) is detrimental to the investment management firm’s bottom line and frequently impacts the portfolio manager’s checkbook. Investment management firms make their money by charging fees, and professional portfolio managers typically make a large portion of their income by retaining and growing the AUM of the product(s) they manage. DeMarche’s thought is that a loss in AUM may precede a period of underperformance, as the lost income for both the firm and the manager may lead to additional changes, distractions, or added risks. The AUM paradox is tricky, however, as we

typically observe an AUM drop following a period of sustained underperformance, as investors grow weary of the poor performing manager.

For the purposes of our study, we considered a “significant” drop in AUM being greater than or equal to a 50% decline in assets over a five-year period. Although imperfect, it’s conceivable that the assets of these products should move upwards with the market (if markets are generally positive, which was the case in the time period examined) and a 50% decline in AUM would properly reflect numerous client-directed outflows. We observed those managers within DeMarche’s Specialty Small Relative Growth and Large Cap Relative Value universes that had performed below median over a trailing three-year period. We then cross-referenced the underperforming products with those that experienced a “significant” loss in assets in the five years preceding the start date of the underperformance. For example, for the three-year period ending March 31, 2020, we looked at AUM losses from the five years prior to March 31, 2017. The results were mixed. Within the DeMarche Large Cap Relative Value universe, just 8% were both underperformers and experienced a significant loss in assets in the three-year period ending March 31, 2020. Similarly, only 5% of the DeMarche Small Cap Relative Growth universe were both underperformers and experienced a significant loss in assets in the five-year period ending March 31, 2020. Looking at AUM in a vacuum did not appear to be a surefire indicator of future underperformance within the DeMarche universes examined. As previously noted and worth repeating, AUM losses typically occur following a period of underperformance or when there is a change in company or product management – more to come on this topic.

For the purposes of our study, we considered a “significant” drop in AUM being greater than or equal to a 50% decline in assets over a five-year period. Although imperfect, it’s conceivable that the assets of these products should move upwards with the market (if markets are generally positive, which was the case in the time period examined) and a 50% decline in AUM would properly reflect numerous client-directed outflows. We observed those managers within DeMarche’s Specialty Small Relative Growth and Large Cap Relative Value universes that had performed below median over a trailing three-year period. We then cross-referenced the underperforming products with those that experienced a “significant” loss in assets in the five years preceding the start date of the underperformance. For example, for the three-year period ending March 31, 2020, we looked at AUM losses from the five years prior to March 31, 2017. The results were mixed. Within the DeMarche Large Cap Relative Value universe, just 8% were both underperformers and experienced a significant loss in assets in the three-year period ending March 31, 2020. Similarly, only 5% of the DeMarche Small Cap Relative Growth universe were both underperformers and experienced a significant loss in assets in the five-year period ending March 31, 2020. Looking at AUM in a vacuum did not appear to be a surefire indicator of future underperformance within the DeMarche universes examined. As previously noted and worth repeating, AUM losses typically occur following a period of underperformance or when there is a change in company or product management – more to come on this topic.

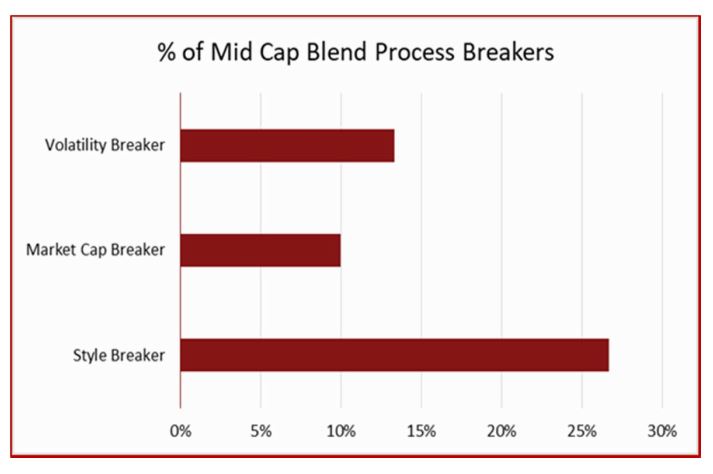

A more subtle leading indicator is categorized as a change in the investment manager’s process or philosophy. While some obvious changes to an investment process certainly exist, many of these changes can go  unnoticed without proper risk and style analysis. While particular changes such as the manager significantly reducing or growing the typical number of investments in a portfolio or implementing a new feature to the investment process are typically well-communicated by the manager, we set out to look for not-so-obvious changes. We used Morningstar to conduct research at this stage, as the data provider assigns an objective investment style and market capitalization score to each product based on numerous underlying quantitative factors. We observed three major buckets of a process/philosophy change within equities: growth-value style change, market capitalization change, and risk budget change. While we understand the measures are not flawless, they are observable in the characteristics of a portfolio over time. For each of the three buckets, we determined a significant style change to be a one standard deviation difference from the average Morningstar Mid Cap Blend variance in scores. In other words, we considered the variation in style, size, and tracking error over a 10-year period, compared that to the average variation of the entire peer group, then observed the products that were on the tails of the normal distribution. We called the products on the tails “process breakers.” In order to tie it all together, we compared these “process breakers” with the products in the fourth quartile amongst Morningstar Mid Cap Blend peers over the trailing five-year period ending March 31, 2020. The results were more significant this time. Of the products in the fourth quartile on a trailing five-year basis, 48% had at least one significant process variation, while 17% had more than one. The most common process breaker was style (growth-value), where over one fourth of the poor performers exhibited significant variation in their style score over a five-year period. Clearly, process and philosophy changes can impact the future performance of a strategy. It is important to ensure any investment strategy under consideration is reflective of the process and philosophy you expect.

unnoticed without proper risk and style analysis. While particular changes such as the manager significantly reducing or growing the typical number of investments in a portfolio or implementing a new feature to the investment process are typically well-communicated by the manager, we set out to look for not-so-obvious changes. We used Morningstar to conduct research at this stage, as the data provider assigns an objective investment style and market capitalization score to each product based on numerous underlying quantitative factors. We observed three major buckets of a process/philosophy change within equities: growth-value style change, market capitalization change, and risk budget change. While we understand the measures are not flawless, they are observable in the characteristics of a portfolio over time. For each of the three buckets, we determined a significant style change to be a one standard deviation difference from the average Morningstar Mid Cap Blend variance in scores. In other words, we considered the variation in style, size, and tracking error over a 10-year period, compared that to the average variation of the entire peer group, then observed the products that were on the tails of the normal distribution. We called the products on the tails “process breakers.” In order to tie it all together, we compared these “process breakers” with the products in the fourth quartile amongst Morningstar Mid Cap Blend peers over the trailing five-year period ending March 31, 2020. The results were more significant this time. Of the products in the fourth quartile on a trailing five-year basis, 48% had at least one significant process variation, while 17% had more than one. The most common process breaker was style (growth-value), where over one fourth of the poor performers exhibited significant variation in their style score over a five-year period. Clearly, process and philosophy changes can impact the future performance of a strategy. It is important to ensure any investment strategy under consideration is reflective of the process and philosophy you expect.

Finally, we turned our efforts to changes in company or portfolio management teams. Ostensibly the most logical leading indicator, a change to key personnel in the establishment and execution of the investment process can introduce significant uncertainty. In the case of a star-system (one key person) - who takes over? In the case where the Lead Portfolio Manager no longer manages the product - how credible and capable are the Assistant Portfolio Manager(s) who will succeed him or her? How about if teams are merged together via an acquisition? What will the team dynamic be moving forward when a key person is no longer involved? What if the firm hires a new CEO/CIO with a markedly different perspective on the investment strategy than their predecessor? All of these considerations are firm or team specific and must be looked at on a case-by-case basis, which is why we did not attempt to quantify management changes in our research for this topic.

For the purposes of the study, we observed every portfolio manager or leadership change noted in our records over the three- year period from 2014 to 2016. We compared those products (or firms) experiencing change with their subsequent performance in the trailing three years ending March 31, 2020. Findings on this were interesting in that there were clear examples where the manager change had an adverse impact on performance, while there were other examples where the change appeared to be positive for performance. In one case, an individual stepped down from their post as Lead Portfolio Manager in order to spend more time with family. Another team-member was promoted to the Lead role from their prior title of Assistant Portfolio Manager, and with guidance from the previous Lead, found themselves in the top decile of performers in their respective category over the subsequent three years. Conversely, there was another example of an extremely similar transition that occurred for similar causes. The previous Director of Research for the firm reduced their responsibilities for personal reasons, and the title was transitioned to another individual on the team. Things weren’t as rosy in this case. The product ended up materially underperforming in the two years following the transition, then subsequently lost nearly 70% of its AUM. While we could go on and on with examples of how manager changes have impacted future performance, the key idea is that there is risk involved with a lack of consistency. It is DeMarche’s opinion that both portfolio management and company leadership changes increase risk of future underperformance; thus these changes need to be addressed and communicated as soon as they occur.

We recognize that just one leading indicator may not result in future underperformance. Although there are numerous examples of multiple issues that exemplify DeMarche’s philosophy, we have chosen the following as it enumerates our thinking.

Firm A had years of stability under their founder, CEO, CIO, and Lead Portfolio Manager. The firm was able to grow AUM significantly over time and managed money for many institutions. Things changed when Firm A’s founder began transferring both the day-to-day portfolio management responsibilities and significant equity in the firm to other employees. The first notable change was the transition in Lead PM duties from the previous “star person” to the new portfolio manager. The new manager had a different portfolio construction approach that included changes to the typical number of holdings and the level of portfolio turnover. Further, DeMarche noted some evidence that more subtle process changes had also occurred. The portfolio previously had a well-defined value style orientation, remained fairly aggressive from a cyclical perspective, and had consistent relative volatility characteristics versus the benchmark. These began to shift after the portfolio was transitioned to the new manager, reaching a point where the new manager’s process and portfolio was nearly unidentifiable from the legacy manager. This example evidenced changes in three leading indicators: a change in organizational structure, a change in lead portfolio management, and process changes. Existing investors subsequently terminated the product after relative performance began to suffer significantly. This scenario happens more often than one may think. Firm transitions are wrought with opportunities to fail gloriously.

It was in staying on top of changes in management at both the firm and portfolio levels, in addition to pulling back the curtain on observing how the process significantly changed at the time of the management transition that we were able to take action and suggest clients terminate the manager.

The leading indicators of future performance are beneficial to the decision-making process for an investment committee. They offer a sense, and sometimes a clearer foreshadowing of potential issues that may impact asset growth and performance. Stability in these indicators helps an investment management firm not only win business, but retain it when discussing performance with their clients in times of style headwinds.

Consider Firm A’s strategy. This strategy had been a relatively stable performer when the former Lead PM had control over the process. It had both up and down years, but relative to both peers and its benchmark, the product was modestly above average. If a client decided to not reallocate their capital at the time of the portfolio manager and process changes, the client would have lost about 4% cumulatively versus the benchmark as of March 31, 2020. Thinking practically, an investor with a $25 million account would have lost $1 million compared to if the investor had earned the benchmark return.

We believe it is paramount that leading indicators to potential lagging performance be monitored in order to protect client capital. In a litigious society where investment committees may be challenged to support their decisions, committees need a workable informed philosophy and framework when considering investment manager selection and retention.