May 2020

Capital preservation strategies

Capital preservation strategies, such as stable value or money market funds are considered to be core investment options and are necessary to meet 404(c) provisions.

Emphasis on quality

The emphasis on the quality of underlying fixed income holdings, investment managers and diversification of wrap providers has placed stable value in a good position to serve as the conservative ballast within a DC plan.

Converting assets to income

In order to help address the chasm between the guaranteed benefits of a DB plan and the non-guaranteed benefits of the DC plan, greater emphasis is now focused on how to actually convert retirement assets to “retirement income.”

In the wake of the Great Financial Crisis (GFC) of 2008-2009, considerable changes took place within the stable value industry. Now a second evolution within stable value seems likely, as Defined Contribution Plans expand their vision to not only focus on accumulating assets but also on decumulation of assets. That is, converting accumulated savings to retirement income. According to JP Morgan’s 2019 Plan Sponsor Survey, 53% of respondents believe plans should be a vehicle for retirement income generation.(1)

Capital preservation strategies, such as stable value or money market funds, are considered core investment options and are necessary to meet 404(c) provisions.(2) In 2019, approximately 78% of DC plans offered stable value options while 63% of plans offered money market options.(3) Stable value is also the first preference for capital preservation funds recommended by consultants.(4) Likewise, many 401(k) plan sponsors use stable value funds as the “safe” option in the plan instead of a money market fund due to their higher historical returns. The income from money market funds depends upon current interest rates and will typically outperform stable value funds only when the yield curve is inverted, which according to the Stable Value Investment Association (SVIA) has happened just 10 times over the past 65 years.(5) According to Pensions & Investments, participant assets allocated to stable value totaled more than $831 billion dollars held across 167,000 different defined contribution plans.(6) Stable value funds provide participants with the “dollar-in/dollar-out” principal protection feature of a money market fund, but with a higher “smoothed” return. Stable value funds are able to generate higher relative returns due to their ability to invest in securities with a maturity of up to four years as compared to the 13-month maturity maximum for money market funds. Stable value funds also provide a smoother return pattern due to their ability to value the portfolio at cost as compared to money market funds which are valued based on daily market values. This smoothing feature reduces the fund’s volatility by allowing funds to amortize gains or losses to the underlying assets over the fund’s duration. Although stable value funds don’t offer the floating net asset value feature of money market funds, they offer market value protection through wrap providers.

A stable value investment contract may “wrap” a portfolio of underlying fixed income securities or guaranteed investment income assets. The wrap providers are typically insurance companies and banks. These wrap contracts guarantee that if the market value of the underlying fixed income portfolio falls below the book value (purchase price) the institution writing the contract will make up the difference if there is a net withdrawal from the fund. The exposure to the wrap provider is diminished as they only pay out the difference of the market price to book value in the event of a net withdrawal where total participant redemptions exceed contributions to the fund.

The Great Financial Crisis caused most stable value funds’ market values to fall below their book values. This was primarily due to aggressive investment guidelines that exposed many stable value funds to the collapse in the credit market. As interest rates had declined, many stable value managers sought higher risk, non-investment grade securities to boost yields. When the financial crisis reached its peak in 2008, the non-investment grade securities were hit particularly hard, causing stable value funds to decline below their book value. As stable value fund portfolios began trading at a discount to book value, the risk exposure of the underlying wrap providers rose significantly, as these providers were ultimately on the hook for the difference. The distress in the stable value industry resulted in more conservative underlying investment guidelines and the need for increased wrap capacity. At this point, the wrap providers transitioned from being dominated by the banking industry that had allowed aggressive investment guidelines and offered low wrap fees (in the 5-10 bps range) to the more conservative approach dominated by a few insurance companies, which required double the wrap fees of banks (in the 20-25 bps range). As the stable value market worked through the GFC, more insurance companies entered the wrap provider market and eventually wrap fees returned to a normalized range of 15-20 bps. The subsequent emphasis on the quality of the underlying fixed income holdings, investment managers and diversification of wrap providers has placed stable value in a good position to serve as the conservative ballast within a DC plan. Stable value is also positioned to provide those in, and nearing, retirement a source of stable income – a commodity much less abundant since the disappearance of traditional defined benefit (DB) plans.

Employees are now relying on Defined Contribution Plans (DC) and social security for critical retirement benefits. In order to help address this chasm between the guaranteed benefits of a DB plan and the non-guaranteed benefits of the DC plan, greater emphasis is now focused on how to actually convert retirement assets to “retirement income.” An idea gaining traction is to implement a “retirement tier” within the DC plan lineup. Investment strategies included in a retirement tier may include managed payout funds, laddered bond strategies, managed account services, annuities, and stable value funds. Stable value funds are considered the strategy that may provide the most consistent income portion of a retirement tier. In this manner, stable value may take a more prominent role within capital preservation needs. According to T. Rowe Price Plan Retirement Services Data, 37% of baby boomers (age 55-73) and silent generation (age 74+) utilize stable value, with an average portfolio allocation of 42% to 59%, respectively.(7)

We also note that plan sponsors are retaining more participants in the plan following their retirement. For example, T. Rowe Price reported that in 2012, 45% of account assets remained in the plan for at least a year after retirement, while 61% of assets remained in 2018.(8) Retirees staying within the plan can reduce costs by capitalizing on the economies of scale of an institutional retirement plan. Because stable value may only be held in tax-qualified plans, such as retirement plans, retirees maintaining an investment in stable value will also be supported by the wider array of institutional retirement services provided by a DC plan. For these reasons, principal preservation offerings play a critical role in the retirement income sleeve or retirement tier of a Plan Sponsor’s Defined Contribution Plan.

However, there are some unique considerations concerning stable value that include the following:

· Equity Wash Rule – A provision within DC plans that limits direct transfers from stable value funds to a “competing fund.” The 90-day equity wash requires participants to transfer money to a non-competing fund, such as equities, for 90 days before moving into a money market fund or short-term bonds. Please note, self-directed brokerage windows may also be considered competing funds.

· Event Risk – Plan-initiated transactions (such as re-enrollment, layoffs, change in plan lineup etc.) would not be at the $1 NAV payout. Stable value funds provide for the payout at $1 per share only for participant directed transfers.

· Wrap Providers – Because a stable value fund is neither insured nor guaranteed by the government, a higher number of wrap providers is generally preferred for diversification of risk.

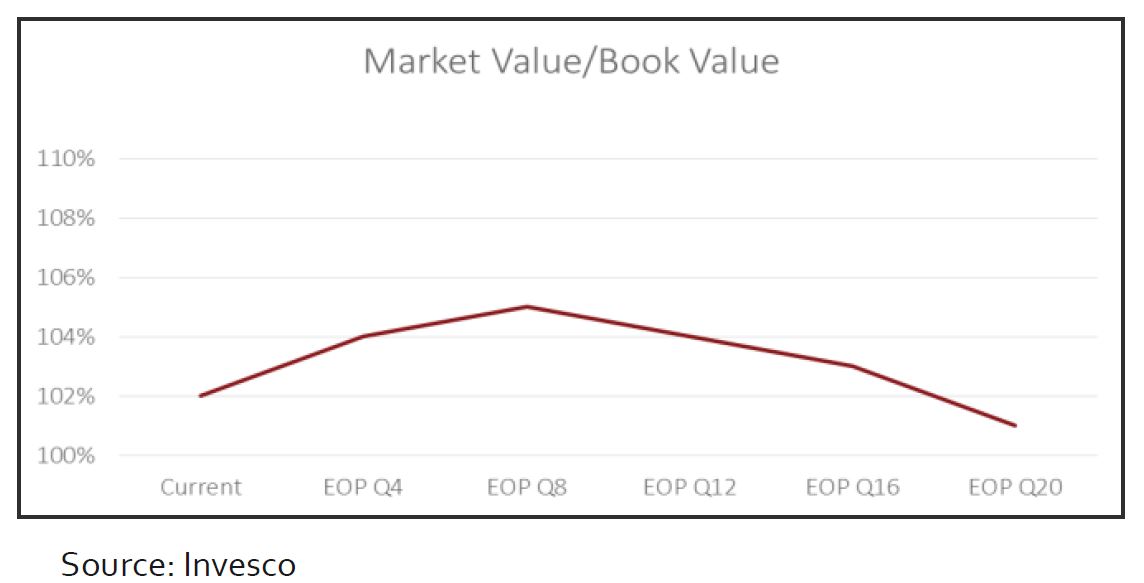

A negative interest rate environment would be another example where the stable value market could come under pressure. Although stable value fund yields would decline in a protracted negative interest rate environment, they would most likely outperform a money market fund due to the stable value fund’s ability to smooth the decline in market value/book values over the duration of the fund. Below is a hypothetical analysis provided by Invesco that incorporates factors that would impact a stable value fund in a negative interest rate environment extending past two years.(9) The factors considered in this example include declining yields, and therefore crediting rates, in addition to declining market value/book values. A stable value fund’s crediting rate is the yield of its underlying investments, minus its wrap and subadvisory costs, plus the market value/book value adjustment amortization over the fund’s duration. Within Invesco’s analysis, it is assumed that the stable value strategy would remain unchanged and would be able to adjust the portfolio based on market conditions. In doing so, the stable value strategy would likely be able to sustain a two-year decline in yields down to earning a negative 75 bps portfolio yield with the crediting rate remaining positive for another three years. Although this scenario is purely hypothetical, it shows how the stable value market’s investment philosophy of maintaining capital preservation would likely remain viable for several years into a negative interest rate environment, allowing plan sponsors and consultants to work through such an event.

During the past two decades, the stable value market has proven the ability to evolve during the most difficult market environments. Stable value managed to maneuver through the Great Financial Crisis in 2008-2009, adapting to necessary investment guidelines changes and a transforming wrap provider lineup. While the current market threatens a decline to portfolio yields, including the possible risk of entering a negative interest rate environment, stable value continues to provide much needed capital preservation within DC plans. Recent increased volatility in capital markets continues to lead to new trends in returns, management and administration that plan sponsors must evaluate in considering the stable value funds utilized in their plans now and in the future. DeMarche Associates, Inc. has assisted clients in their evaluations of their stable value funds and other 401(k) offerings since the 1980.