July 2020

Benjamin Graham's The Intelligent Investor is an often-recommended book in the investing world, a fit for both beginners and those with great experience. Graham's philosophy centers not on the maximization of gains but on the avoidance of large losses over the long term. One quote stands out from the text for institutional investors:

"The beauty of periodic rebalancing is that it forces you to base your investing decisions on a simple, objective standard." - Benjamin Graham

Periodic rebalancing is a widely accepted idea, but why does the institutional investor take time to re-allocate assets? Assuming a two-asset portfolio for the sake of simplicity, the first thing one must look at is the innate equity premium relative to fixed income. Comparing returns of fixed income relative to equity, equity is inherently more volatile but higher returning (10.3% vs. 5.3% annually over the last 70+ years) and, as a result, will increase in proportion to the underlying allocation over the course of multiple market cycles. An investor who starts off with a simple 65% equity/35% fixed income allocation with a buy-and-hold approach may find themselves with a completely different allocation over the course of multiple market cycles, likely with a substantial overweight to equity. The outcome as a result of this shift is a change in the underlying characteristics of the asset allocation mix, and a portfolio which previously may have been suited in terms of return and risk characteristics is now ill-suited for that same client. The final possible benefit of rules-based rebalancing is the removal of the human element and possible non-optimal behavior. By sticking to a systematic approach to rebalancing the asset allocation mix, the risk of "buying high and selling low" is reduced via an orientation towards reversion to the mean.

Strategies to implementation of rebalancing can be described as falling into three distinct camps based on the factors considered: time-only, threshold-only, and time-and-threshold. In time-only approaches, rebalancing is done on a set schedule, whether it be weekly, monthly, annually or any other time frame. This approach pays no mind to the magnitude of asset allocation shifts in-between the set time intervals. In threshold-only approaches, the only variable taken into account is deviation from set parameters, and changes are made only when the portfolio differs by a set increment (5%, 10%, etc.) from the target allocation. This approach requires continuous monitoring of the portfolio and is often difficult to implement. The time-and-threshold approach is based on a set time schedule for monitoring, but changes are only made once the asset allocation mix differs by a predetermined amount from the target mix.

etc.) from the target allocation. This approach requires continuous monitoring of the portfolio and is often difficult to implement. The time-and-threshold approach is based on a set time schedule for monitoring, but changes are only made once the asset allocation mix differs by a predetermined amount from the target mix.

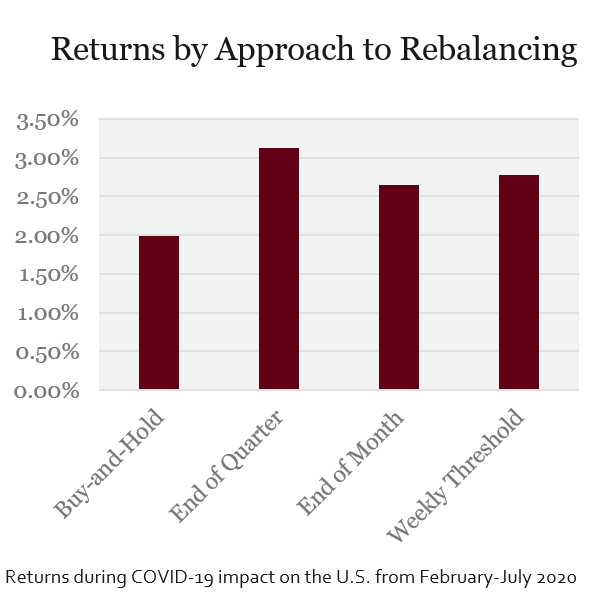

One recent example of the benefits to rebalancing regularly came this year in the market decline post-February, following the COVID-19 outbreak and subsequent decline and recovery in the equity markets. As shown to the right, there are three common courses of action which investors took during this period: a buy-and-hold approach, rebalancing on a monthly/quarterly basis and rebalancing when weekly allocations differed from a policy guideline. The most successful approach for a sample 65/35 portfolio in this period was rebalancing (no matter the timing), similar to other comparable market declines and recoveries, such as the dot-com bubble and Global Financial Crisis. The passive ("buy and hold") strategy failed to outperform over the period and has historically been a relatively poor approach in comparison.

An analysis done by Vanguard Research showed that monthly and annual rebalancing for portfolios has historically been a sound strategy. When looking at returns for a portfolio of 50% global stocks/50% global bonds over the course of 88 years of market data, and a 5% threshold of deviation, annual rebalancing produced an 8.2% average annualized return with a 9.8% annualized volatility in comparison to a "buy-and-hold" approach, which produced an 8.9% average annualized return but with a significantly higher annualized volatility of 13.2% resulting from the increased allocation to equity over time. Since 1972, the strategy of mean reversion has outperformed momentum-based/hold-based strategies over the course of time. Selling high and buying low has consistently worked over the past 38 years, which Factor Research believes is the result of four historical changes in the marketplace: an expansion of futures trading markets by the Chicago Board of Trade (CBOT), an ever-increasing level of institutional asset management, higher synchronization of global capital markets and increasing competition in trading fees leading to better outcomes for participants. The strength of mean reversion has translated into better outcomes for those with rules-based rebalancing approaches. In ever-turbulent markets, smoothing out the ride and potential outcomes for investors has never been more important. For more information on applying this study and how DeMarche approaches asset allocation and portfolio rebalancing, please contact your DeMarche Consultant.